Finnish Real Estate Market - Q1 2026

The first quarter of 2026 confirmed that the real estate market recovery is continuing. Transaction volume rose to exceptionally high levels, driven by a single large residential portfolio transaction, but activity was visible across several segments. The Middle East conflict is the key variable for the remainder of the year.

Key takeaways – Q1 2026

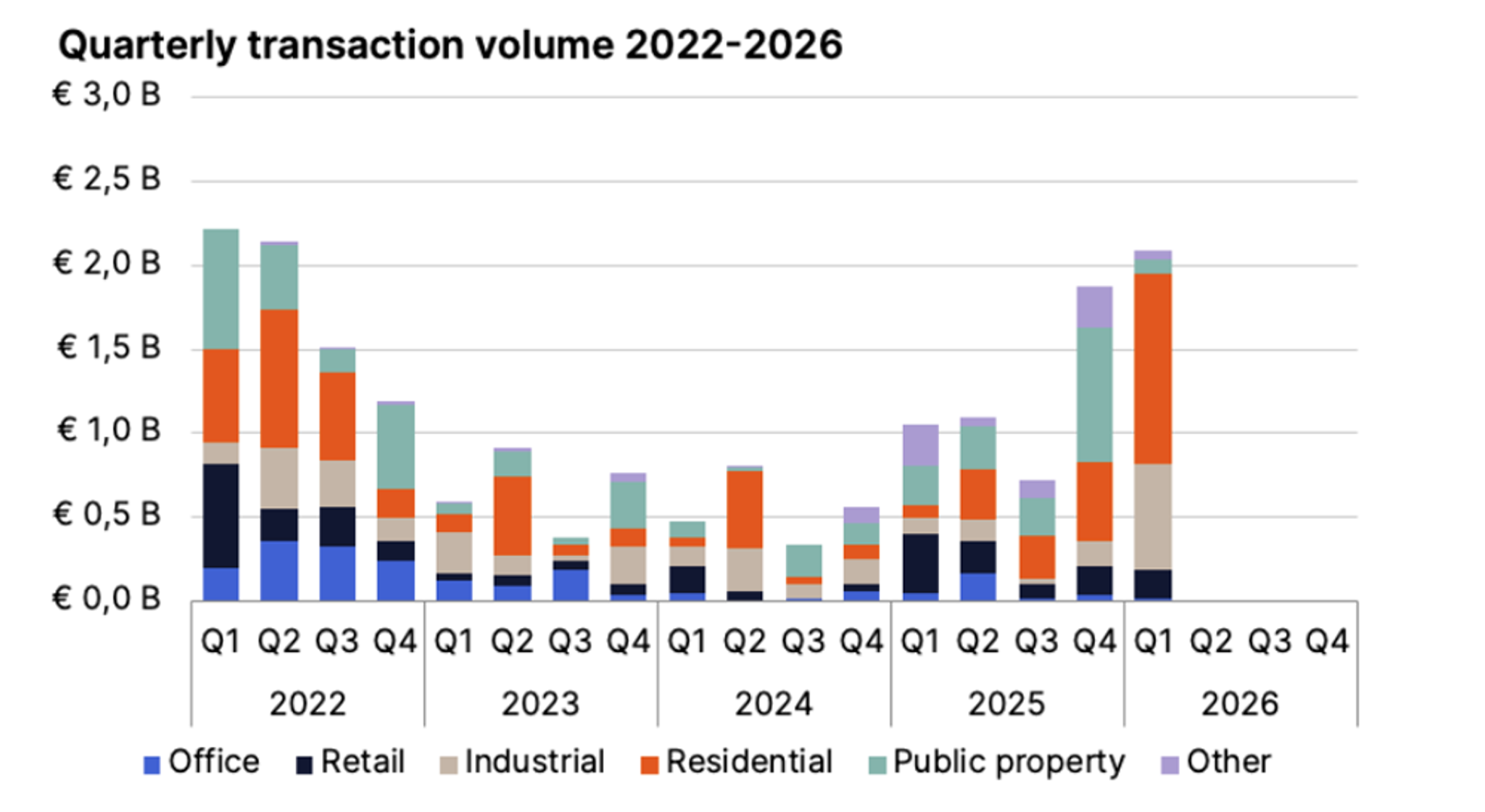

- Historic transaction volume: The Q1 2026 total volume rose to exceptionally high levels, driven by the approximately EUR 900 million residential transaction between Varma and Kojamo (now Lumo Kodit). The residential segment recorded its highest-ever quarter, and the industrial and logistics segment its second-highest on record.

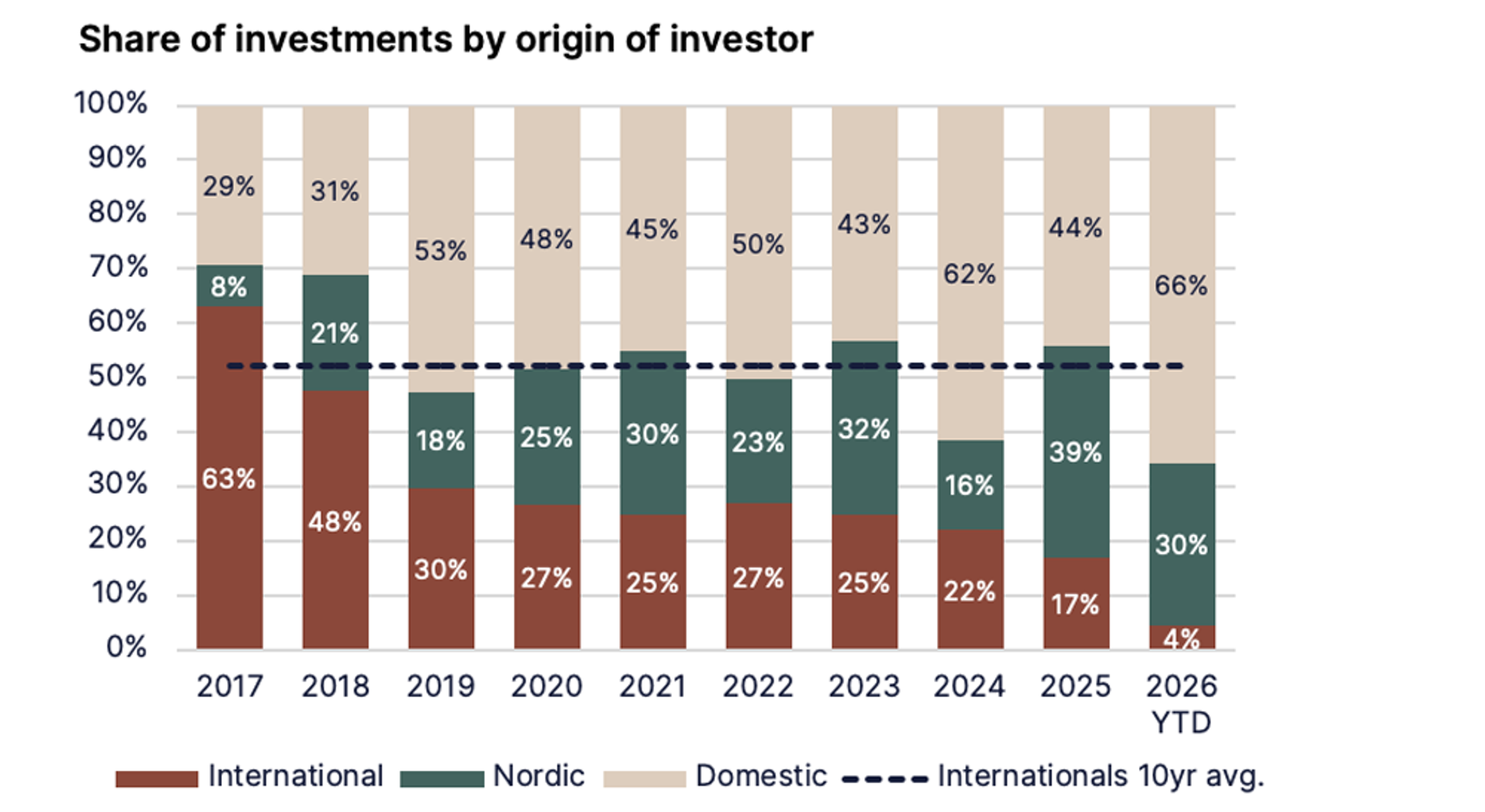

- Nordic investors active: The share of international investors remained high. In the industrial and logistics segment, the share rose to almost 90%, and Swedish investors continued to be active both in that segment and in the retail market.

- Polarisation deepens: Investor demand is concentrated selectively on specific segments: residential, logistics, grocery-anchored retail, and public properties. The office market continues to await a broader turning point.

- Macroeconomic uncertainty rising: Energy inflation triggered by the Middle East conflict has shifted interest rate expectations upwards, limiting further compression in prime yields.

Recovery continues, but the Middle East conflict casts a shadow

The operating environment has changed rapidly during the early part of the year. The Middle East conflict has accelerated energy inflation, lifted interest rate expectations, and weakened growth forecasts. The same uncertainty that defined 2025 continues, but investors are still actively seeking assets in segments underpinned by strong fundamentals.

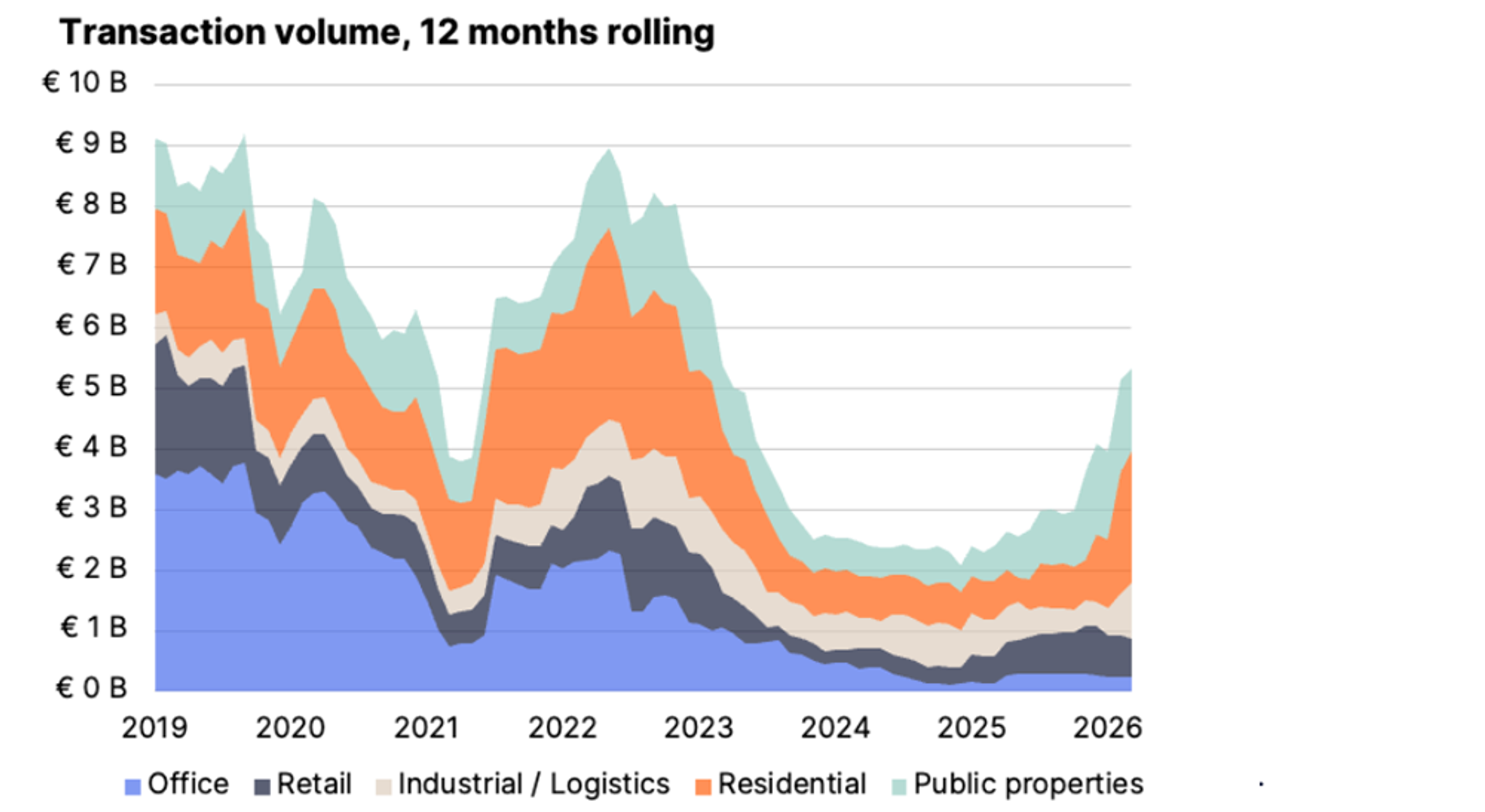

Q1 2026 residential transaction volume rose to historically high levels, driven by a single large residential portfolio transaction, but activity in the early part of the year was visible broadly across segments. The industrial and logistics quarter was the second-highest on record, and retail transaction activity continued at an established level. Office market volume remained subdued.

The large transactions in the early part of the year reflected the same broader investor demand seen elsewhere in Europe. Kojamo acquired nearly 4,800 apartments from Varma for approximately EUR 900 million, one of the largest single transactions in the history of the Finnish real estate market. Sweden's Catena acquired a portfolio of seven logistics assets from Urban Partners for approximately EUR 197 million, and Stendörren acquired 14 warehouse and light industrial properties from the Sjöblom family for EUR 123 million. On the retail side, Nordisk Renting acquired Kesko's K-Citymarket scheme in Oulu for approximately EUR 50 million.

International investors keep liquidity flowing

International capital continues to play a central role in supporting liquidity in the Finnish real estate market. With domestic open-ended funds and pension investors remaining predominantly on the sell-side, foreign investors, particularly Nordic and especially Swedish players, have actively capitalised on the buying opportunities. The overall share of international investors in Q1 was 34%, but in the industrial and logistics segment, the share rose to almost 90%.

Finland has retained its position as a target market for international investors. In Nordic comparison, intensifying competition in Sweden has boosted interest in Finnish retail and logistics assets, where yields and entry thresholds are attractive. From the broader European real estate market perspective, the residential and logistics segments have remained at the top of allocations for institutional investors and lenders alike.

Domestic institutional investors remain predominantly on the sell side this year. This continues to create clear buying opportunities, which are being capitalised on by both large domestic players and international investors with the ability to act quickly and at scale.

Segment-by-segment development: winners and those waiting

Transaction volumes for 2025 and Q1 2026 clearly show which segments are leading the market. Residential, logistics, grocery-anchored retail, and public properties are at the top of the demand list. What these have in common is long cash flows and/or structural demand drivers.

In the residential market, the supply cycle has turned. New construction in the Helsinki Metropolitan Area will contract through 2028, occupancy rates are recovering, and oversupply is being absorbed. The situation is not yet visible in rents, but we expect a shift from next year onwards. In logistics, transaction activity was exceptionally strong, even though vacancy has risen. Structural drivers continue to support investor conviction over the long term, and prime properties and locations are attracting tenants. In the retail market, grocery-anchored retail and big-box properties are defensive assets that have performed strongly even in the challenging consumer environment.

The office market continues to await a broader turning point. Total vacancy in the Helsinki Metropolitan Area rose to 15.3%, but the polarisation is visible: vacancy in CBD Grade A offices stood at 5.8%, and leasing activity is effectively at a post-pandemic high. A broader recovery in the investment market will likely require the return of international investors, who have been absent from the office market for more than three years.

Interest rates turning, risk premium narrowing

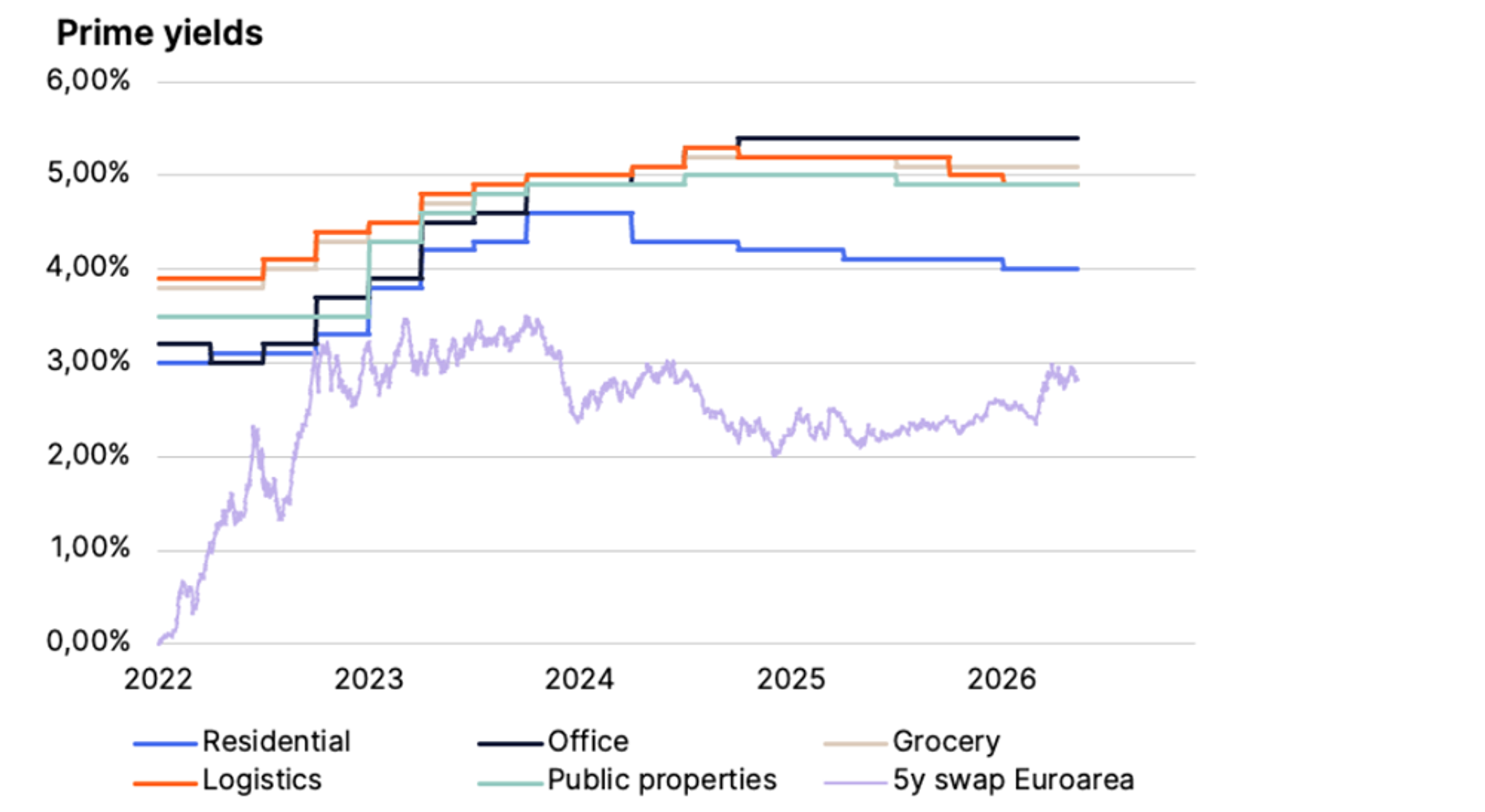

The Middle East conflict has rapidly shifted the outlook for monetary policy. The ECB held its deposit rate at 2.0% in April, but markets are now pricing in rate hikes for the remainder of the year. Nordea expects the deposit rate to rise to 3% by the end of 2026. Energy inflation is the central driver.

Long-term market rates have risen, lifting the cost of corporate debt financing and feeding through directly into real estate investment yield requirements. Financing availability for prime assets nonetheless remains strong; banks are active, and margins have held steady at modest levels for high-quality assets. Residential and logistics properties remain among the most favoured sectors for debt financing.

Newsec's Q1 prime yield forecast for 2027 indicated modest compression across the main segments, but elevated risk-free rate expectations now impose constraints. We produce the yield forecast quarterly, and the next long-term forecast will be issued in May.

Looking ahead

Q1 2026 confirms that the Finnish real estate market continues in a recovery cycle, but the cycle will progress selectively from here. The strong segments are attracting capital, the office market is awaiting a turning point, and geopolitical uncertainty is keeping predictability challenging. The duration of the Middle East conflict and its impact on energy prices and interest rates are the key variable for the remainder of the year.

Newsec expects transaction volume to continue growing in 2026, as domestic capital gradually reactivates and international demand remains strong. The ongoing recovery cycle, however, is still shadowed by several factors, and the recovery steps remain cautious.

The reports below contain more detailed information on segment-specific developments in the most recent quarter.

Newsec Industrial and Logistics Q1/2026

Newsec Public Properties Q1/2026

More information:

Valtteri Vuorio

Head of Research,

Newsec Advisory in Finland

valtteri.vuorio@newsec.fi

+358 40 705 3093

The downloadable market reports contain key data on the previous quarter's real estate market. More detailed information by segment and sub-market is available in Newsec's subscription market reports. Newsec provides the most comprehensive data in Finland on the residential, office, and logistics markets. For more information, please contact markkinakatsaukset@newsec.fi.

Yksityiskohdat

Julkaisupäivä

260512

Muoto

Kieli

English